Exploring Chapter 13 Bankruptcy & Its Impact On Student Loans

Student loans can be overwhelming, especially if you have other debt weighing you down. You might find yourself in some challenging situations, facing lawsuits, collections harassment, and wage garnishments. You might be desperate to find a path towards more financial freedom. Chapter 13 can be a helpful tool in getting you there.

Unfortunately, student loans are generally nondischargeable, but working with your bankruptcy lawyer can help you significantly reduce other debts and improve your financial situation. Benefiting from an automatic stay, a 3-5 year affordable payment plan, and the discharge of some debts can leave you in a much better financial situation than you were before. It can allow you to stay on top of remaining student loans and move forward with more financial freedom.

This blog will help you better understand how Chapter 13 can be a positive choice when you’re overwhelmed by student loans.

Different Types Of Student Loans You May Owe

College is expensive and student loans are necessary for many individuals. There are several different types of student loans you can get to help pay for higher education. However, when it comes to bankruptcy, student loans are generally all treated the same. The options of loans include:

College is expensive and student loans are necessary for many individuals. There are several different types of student loans you can get to help pay for higher education. However, when it comes to bankruptcy, student loans are generally all treated the same. The options of loans include:

- Federal student loans

- Private student loans

- State or institutional loans

Why Student Loans Are Not Dischargeable With Bankruptcy

While bankruptcy is known to wipe out debts, it does not wipe out every type of debt. Many debts are referred to as nondischargeable. Unfortunately, student loans fall under a nondischargeable debt. It is possible to have them discharged in rare circumstances by proving you’re unable to pay due to “undue hardship”, but most people do not qualify.

However, just because a debt is nondischargeable doesn’t mean that bankruptcy cannot play a helpful role in paying it back. Talk with a Honolulu bankruptcy lawyer to start the process of filing for bankruptcy and see how it might benefit you.

How Chapter 13 Bankruptcy Can Impact Student Loans

Filing for Chapter 13 bankruptcy can be a great chance to start over if you’re drowning in student debt and other loans. Some of the impacts this type of bankruptcy can have on your student loans include:

- Stops collection actions and wage garnishments

- Consolidates debts into one affordable debt payment

- Takes care of priority and secured debt, so you have less to manage once bankruptcy is complete

- Provides a 3-5 year break in debt to stabilize your finances.

How Student Loans Are Handled In Chapter 13 Bankruptcy

When you file for Chapter 13 bankruptcy, you will experience an automatic stay that halts any collection contacts or actions, including wage garnishments. You will work with a bankruptcy lawyer to draft a 3-5 year repayment plan on all your debts that is within your means to pay and is one consolidated payment. The automatic stay will be in place throughout the duration of this plan.

Your payment plan must be approved by the bankruptcy court and you will pay the affordable monthly payment to your bankruptcy trustee, who will use the money to pay off creditors. Once the 3-5 year plan is over, eligible debts will be discharged and nondischargeable debts will continue to require payment.

While Chapter 13 bankruptcy will not discharge your student loans, it does consolidate your debt payments into something manageable for 3-5 years without penalty from the creditor. During this time, you might have the opportunity to find other ways of securing more income to pay debts.

What Happens To Student Loans After Chapter 13 Bankruptcy Is Over?

It’s important to consider what happens to your student loans once Chapter 13 bankruptcy is complete. If your loan amount was small enough, the bankruptcy plan may have taken care of the full amount. However, if they are not paid off, you will be required to continue paying these loans once your 3-5 year plan is complete.

It’s important to consider what happens to your student loans once Chapter 13 bankruptcy is complete. If your loan amount was small enough, the bankruptcy plan may have taken care of the full amount. However, if they are not paid off, you will be required to continue paying these loans once your 3-5 year plan is complete.

During your bankruptcy plan, collections actions are halted, but interest can still accrue. This can result in more money owed after the plan than was owed before the plan. Additionally, once the plan is over, collection actions can begin again. Your bankruptcy lawyer can walk you through the best course of action to protect yourself before the automatic stay is removed.

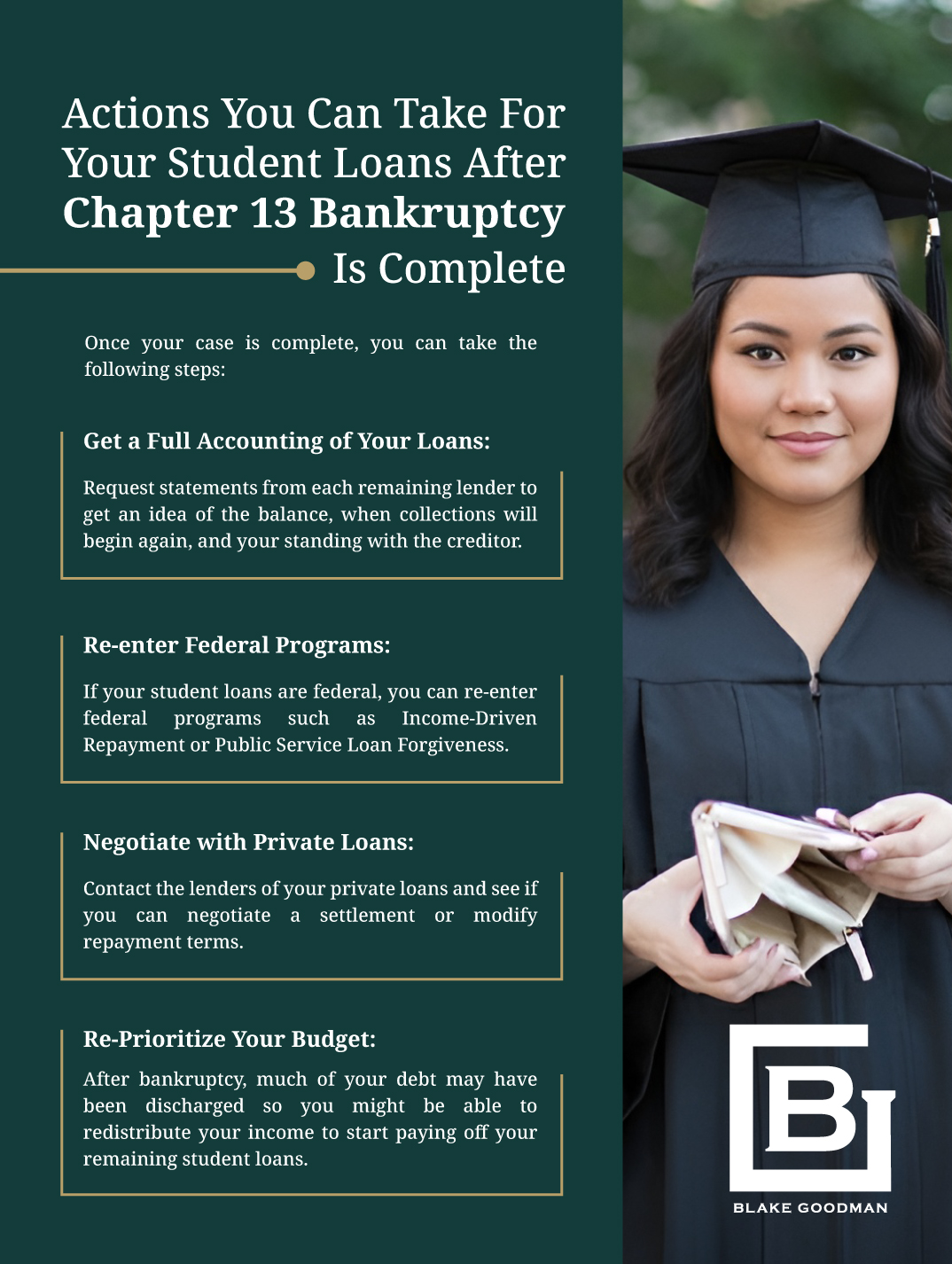

Actions You Can Take For Your Student Loans After Chapter 13 Bankruptcy Is Complete

Once your case is complete, you can take the following steps:

- Get a Full Accounting of Your Loans: Request statements from each remaining lender to get an idea of the balance, when collections will begin again, and your standing with the creditor.

- Re-enter Federal Programs: If your student loans are federal, you can re-enter federal programs such as Income-Driven Repayment or Public Service Loan Forgiveness.

- Negotiate with Private Loans: Contact the lenders of your private loans and see if you can negotiate a settlement or modify repayment terms.

- Re-Prioritize Your Budget: After bankruptcy, much of your debt may have been discharged so you might be able to redistribute your income to start paying off your remaining student loans.

File For Chapter 13 Bankruptcy With The Help Of Our Trusted Honolulu Bankruptcy Lawyers & Move Towards Financial Freedom

If you are drowning in school loans, our Honolulu bankruptcy lawyers at Blake Goodman can help. We will look over your financial situation and help you determine the best repayment plan for your case in Chapter 13 bankruptcy. You can rely on us to protect your rights and walk you through every step for the best outcome possible.

Reach out to our lawyers today and discover how you can make significant steps out of your debilitating debt.

Email: blake@debtfreehawaii.com

Website: https://www.debtfreehawaii.com/

HONOLULU OFFICE

900 Fort Street MallSuite 910

Honolulu, HI 96813

Phone: (808) 517-5446

AIEA OFFICE

98-1238 Ka'ahumanu StSuite 201

Pearl City, HI 96782

Phone: (808) 515-3441

KANEOHE OFFICE

46-005 Kawa StSuite 206

Kaneohe, HI 96744

Phone: (808) 515-3304

MAUI OFFICE

220 Imi Kala St. #203BWailuku, HI 96793

Phone: (808) 515-2037

Blake Goodman received his law degree from George Washington University in Washington, D.C. in 1989 and has been exclusively practicing bankruptcy-related law in Texas, New Mexico, and Hawaii ever since. In the past, Attorney Goodman also worked as a Certified Public Accountant, receiving his license form the State of Maryland in 1988.